Failure.

Failure hurts.

Watching something you’ve poured endless amounts of time and energy in, only to see it crumble before you will hurt like hell. It’ll be like a physical punch to the gut, and it will paralyze you. It’s no wonder that entrepreneurs avoid failure like the plague.

A startup can go under for a variety of reasons. While founders can stand around and point fingers at each other, attribute it to forces outside of their control, or just blame bad luck. The reality is that startup failure is from a refusal to acknowledge problems until the ship is already sinking.

The reality of the situation is you are more likely to fail than you are to succeed. If you’re defining startup failure as the inability to deliver on the projected return of investment, then 95% of startups are failures.

But there is no greater teacher than failure.

If you’re going to be an entrepreneur then you better get used to failing, it will become an inevitable part of your life. Don’t run from it, embrace it, and see what lessons you can learn from it.

By analyzing the post-mortems of various failed startups here are the expected and not-so-expected reasons why they failed and what you can learn from their mistakes. Watch out for those icebergs.

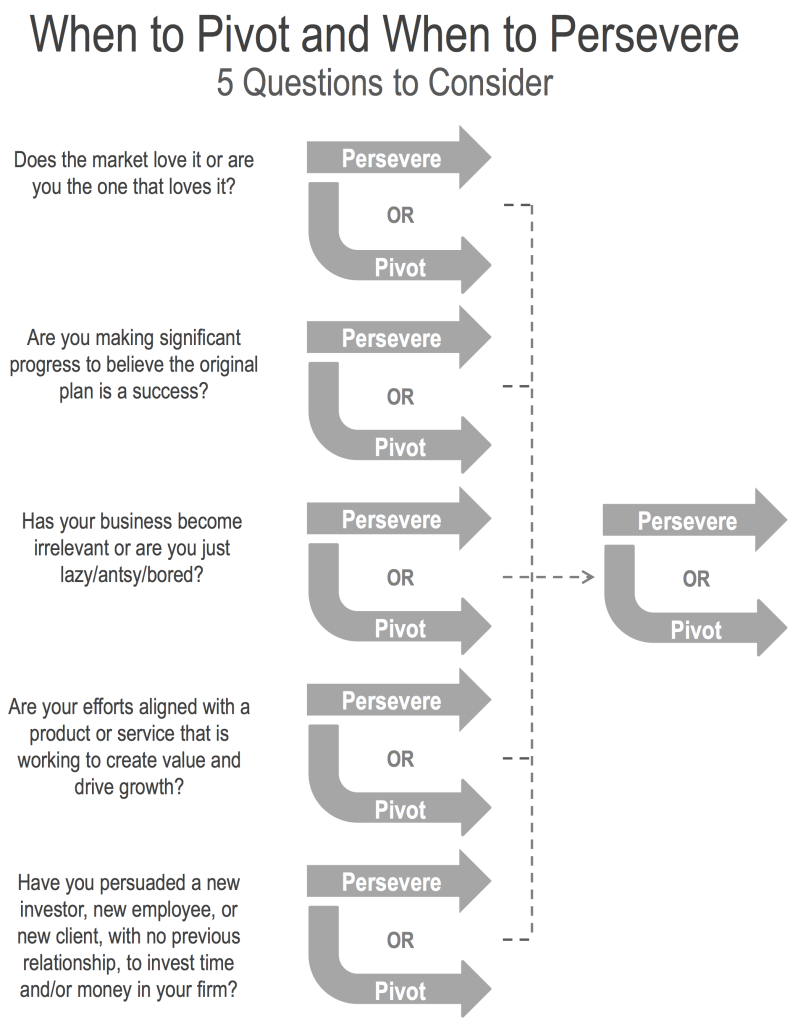

Be Wary of the Pivot

Fab was once known as ‘the world’s fastest-growing startup’ and was valued at over at $1 billion before it ultimately crashed.

Fab underwent a variety of changes from an LGBT social network, to a daily flash sales site, to ‘the world’s design store’, before finally being sold off to PCH, for a reported $15 million in cash and stock.

Fab is both a success story and a cautionary tale to entrepreneurs about the risks of pivoting. A pivot generally means that a business is looking to find a fresh perspective and vision to prevent itself from growing stagnant.

Hypothetically a startup should constantly be evaluating data: measuring the market, contemplating new strategies, testing new products. A pivot allows a business to forge ahead in a new direction when either the opportunity is clear, or the current strategy is failing.

“Once we made the decision to pivot, we committed to doing one thing and doing it well. No distractions.” – Jason Goldberg, cofounder and CEO of Fab.

Fab was originally known as Fabulis an LGBT social networking site before pivoting wonderfully into a daily flash sales site for independent artists. Cofounders Jason Goldberg and Bradford Shellhammer admitted to themselves that Fabulis wasn’t turning out to be the success that they hoped, being stuck at 150,000 users for the last few months. It was time to pivot.

The data they had gathered from Fabulis illuminated a real hole in the design market. People were looking for an easy and accessible way to purchase unique and interesting designerwear.

So, they pivoted and became a daily flash sales site for designer housewares, accessories, clothing, and jewelry. The move paid off with Fab growing to over 10 million users and reportedly generating more than $200,000 every day.

Two years later after the initial pivot, despite a shaky business model, Fab decided to pivot again. This time looking to become a designer alternative to Amazon and IKEA. Coupled with a failed attempt to expand into the European market, Fab began its spectacular fall.

READ MORE: Is Your Business Not Making Enough Money? Here’s How to Fix It

The first and foremost requirement for a pivot to truly succeed is it must solve a major problem. At the time Fab was a hugely successful company, despite the fact that the daily flash sales model wasn’t sustainable in the long-term, choosing to drastically scale down their product offerings moved too far from their identity as a designer store. Fab ultimately created another problem while prematurely trying to solve another.

It’s only natural for a struggling startup to pivot, especially when the alternative is to remain stagnant and unprofitable. However as Fab demonstrated, pivoting for the sake of pivoting, or to expand on a shaky business model will almost always guarantee disaster for any entrepreneur out there. No matter how much money you’ve raised.

READ MORE: How Competitive Collaboration Can Boost Your Business

Too Ambitious, Too Fast

Webvan was the biggest flop during the dotcom era of startups.

Webvan was the biggest flop during the dotcom era of startups.

At its peak, in 1999, it was valued at $1.2 billion. Two years later they filed for bankruptcy, laid off 2000 employees, and closed up shop. Webvan could potentially be considered a startup ahead of its time, their vision was a home-delivery service for groceries, where customers could order their groceries online, but that’s not where the problem lies.

15 years later it’s still being studied by business schools around the world as a forewarning against excess and ambition.

Webvan can also be considered a product of its time, the result was that it followed the ‘Get Big Fast’ (GBF) business model that every other startup was religiously following at the time. In 1999 Webvan announced they would expand to 26 major cities.

The following two years became a logistical nightmare with Webvan ultimately losing a total of $830 million before filing for bankruptcy.

“Webvan committed the cardinal sin of retail, which is to expand into new territory before we had demonstrated success in the first market. In fact, we were busy demonstrating failure in the Bay Area market while we expanded into other regions,” said Mike Moritz, former Webvan board member, and partner at Sequoia Capital.

READ MORE: How to Make Money With Your Email List

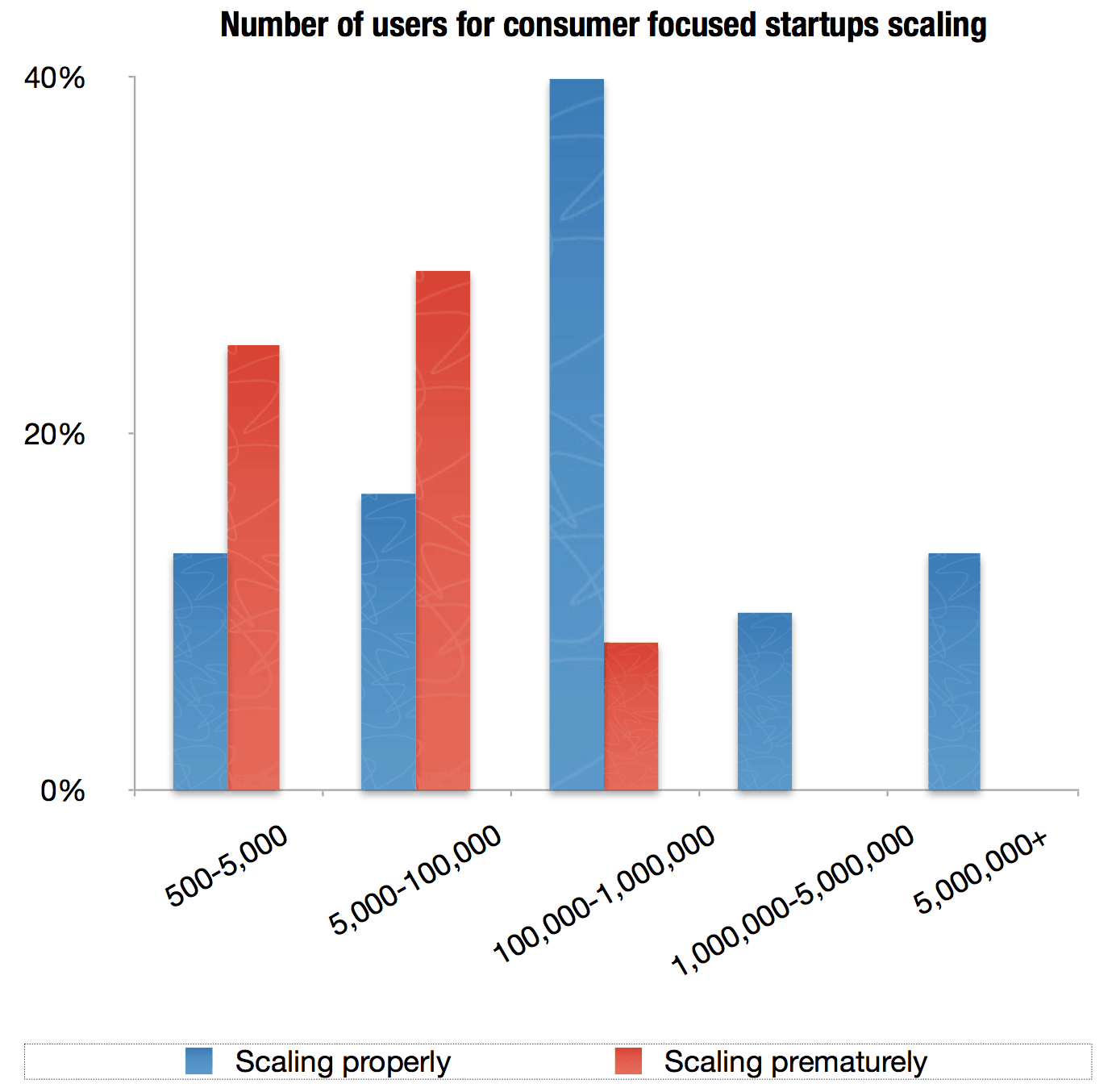

At some point, every successful startup will have to start scaling up and expanding their business. It seems like common sense, but expansion should only be undertaken when a business model has first proven to be successful.

A few rules of thumb are that a scalable business model should be flexible to be able to adapt to different market conditions, core users and customers are evaluated and understood, and the business model should be able to operate without your direct supervision. Common sense right?

Yet according to the Startup Genome Project’s survey of over 3200 startups, 74% of startup failures can be attributed to premature scaling. Another key finding was that startups, on average, need 2-3 times longer to validate their market than the founders expect. This underestimation of appropriate timelines applies unnecessary pressure on founders to scale prematurely.

Despite early validation, Webvan failed to consistently evaluate the data. If they had paid closer attention then they would’ve seen that their business model was shaky and could not possibly support their desired plans for expansion.

It’s only natural for entrepreneurs to want to grow their business. But as Webvan learned, it’s important to grow your business for the right reasons. To pay attention to the data at hand, and never grow for the sake of growth.

Be Wary of Who You Get in Bed With

Many readers will be familiar with The Muse an online business dedicated to helping female entrepreneurs by offering mentorship, advice and career opportunities. What you probably won’t be familiar with is Pretty Young Professional the predecessor to The Muse and Kathryn Minshew’s first startup that fell apart due to bad communication, legal issues, and infighting among the team.

Many readers will be familiar with The Muse an online business dedicated to helping female entrepreneurs by offering mentorship, advice and career opportunities. What you probably won’t be familiar with is Pretty Young Professional the predecessor to The Muse and Kathryn Minshew’s first startup that fell apart due to bad communication, legal issues, and infighting among the team.

Pretty Young Professional was founded by four colleagues at McKinsey, a global consultancy firm, who noticed the lack of resources for young women in the world of entrepreneurship.

It had a simple vision, to provide a weekly newsletter and cultivate a community for young female entrepreneurs. All four were coworkers, friends even, who shared a similar passion and vision. A meeting was held; positions and equity were decided amongst themselves and written on a notepad. And that’s when the trouble began.

READ MORE: How to Build a Profitable Marketing Strategy

Kathryn Minshew, co-founder, and CEO of Pretty Young Professional said that “it came down to some pretty fundamental differences of opinion around where the business should be heading. I think, naively, we assumed that if we kicked the can down the road on some of those things, we’d be able to sort them out.”

Despite the years you’ve shared together and the many years of in-jokes you have, conventional wisdom dictates that it’s a bad idea to mix business with friends.

A study by the University of Auckland Business School found that while maintaining strong friendships with co-workers generally improves work productivity and morale it also creates a dilemma when trying to reconcile personal relationships with professional decision-making.

In business, it’s required that you have to make the logical and necessary decisions in order to benefit your company, even at the cost of personal friendships.

11 months in, the four founders of Pretty Young Professional had split into two camps due to differences in opinion, and a coup was staged. The legality of the original document was called into question, Minshew was hit with a lawsuit and called to step down as CEO, and the editorial team of Pretty Young Professional had their site and email access cut. The company quickly collapsed despite calls from excited investors and a thriving user base.

While it is possible to work with friends and family, it requires completely honest communication, both parties must understand that it really is nothing personal, and, perhaps most importantly, vest your ownership. It’s always best practice to ensure that you legally protect yourself and your assets, a promise between friends rarely holds up in the court of law.

READ MORE: 5 Best Sales Funnel Software Tools to Power Your Business

The Double-Edged Sword of SEO

Tutorspree was launched in 2011 out of startup incubator Y Combinator and was touted as the ‘Airbnb of tutoring’.

Tutorspree was launched in 2011 out of startup incubator Y Combinator and was touted as the ‘Airbnb of tutoring’.

The premise was simple, to help parents find tutors for their kids online. By 2013 they had over 7000 tutors signed up on their platform and has raised an estimated $1.8 million. Then the rug was swept out from under then and they closed down a few months later, after 3 years in operation.

It appeared that Tutorspree was doing everything right, it had managed to raise an impressive amount of capital from heavyweight investors like Sequoia Capital and Lerer Ventures. They were scaling at a decent pace, albeit not as fast as they wanted, and the business model was proving to be profitable.

However, it fell apart in March of 2013 when Google changed its algorithm and Tutorspree found their traffic reduced by 80% overnight. While this normally wouldn’t cripple a business, it was a catastrophe for Tutorspree. SEO was baked into their business model from the very start and almost all of their customer acquisitions originated from SEO.

“Nor is the largest lesson for me that SEO shouldn’t be part of a startup’s marketing kit. It should be there, but it has to be just one of many tools. SEO cannot be the only channel a company has, nor can any other single-channel serve that purpose.” – Aaron Harris, co-founder, and CEO of Tutorspree.

READ MORE: How to Develop Powerful Business Core Values and Mission Statements

There are many different types of SEO practices, but SEO is essentially improving the visibility and authority of a website by having it rank higher on search engine listings. The entrepreneurial community itself is very divided on the merits of SEO.

The issue with Tutorspree wasn’t whether or not it used SEO effectively or ineffectively. The issue was that due to its effectiveness, the founders became blind to other models of customer acquisition and developed an overreliance on a model they had absolutely no control over.

Google’s algorithm constantly changes and there’s no telling how it will ultimately affect your website’s ranking. Google has consistently proven to burn anyone that chooses to rely on SEO as their main strategy.

It should go without saying that you shouldn’t be putting all your eggs into one basket. Entrepreneurs should invest half their marketing into a high-risk strategy, and the other half in a proven consistent strategy, albeit with a lower return on investment. When it comes to business, you can either live or die by the sword or just be smart and carry a shield.

READ MORE: Building the Perfect Sales Funnel for Your Shopify Store

Summary

Failure is difficult to handle, but there is no better teacher. Although every business listed failed spectacularly, all of their founders got back up, dusted themselves off, and forged ahead to eventual success.

While it’s easy to see all the mistakes you made in hindsight, don’t let yourself get to that point. Failure can be seen a mile away if you’re paying close enough attention, even if it means asking yourself some uncomfortable questions. A lot of businesses could have been saved if just the smallest amount of preparation was undertaken, or if founders had just a little bit more patience.

Is there a bigger startup failure that you’ve heard about? We love case studies! Let us know in the comments below.